Two-year anniversary update

A belated post; sorry for the hiatus!

JTK and AC/PC are cofounders of Relation and Entelo Bio, respectively, which use many of these platforms. scTrends does not reflect the opinions of any affiliated employers, and we try to stay data-driven and flag where we editorialise. JTK: Apologies for the delay, it’s been busy at Relation with deals announced (see Novartis announcement), but also new progress soon hitting the public domain.

Two years on from launching scTrends (see original commentary & review), the field has done what we hoped it would — moved fast enough to make a living review worth maintaining. This update covers what has changed commercially since our previous posts, covering roughly January 2025 through June 2026. As always, our bar for inclusion is a product you can actually buy or order as a service, not academic work.

If you want to skip the news and just see an up-to-date version of the technology comparison spreadsheets: link here (apologies if no immediate access, fixing IT security issues).

Side note: whilst we have used agents to identify news stories (we did this manually initially!), the interpretation (see “the scTrends take” is our own.

Technology news

The whole-transcriptome spatial arms race

If pre-2024 was about plex — how many genes your panel can hit — then 2025–26 is about dropping panel design altogether and going transcriptome wide.

Imaging-based spatial transcriptomics

Summer 2025 — Bruker (ex-NanoString) CosMx Whole Transcriptome (WTX): >18,000 genes, subcellular, on FFPE — the imaging-based answer, and arguably the most direct pressure on Xenium’s panel franchise.

FEB26 — Singular Genomics launched G4X in the US, repurposing the optics and sequencing-by-synthesis chemistry of its (commercially underwhelming) G4 sequencer as an in-situ readout. The pitch is multiomics on a single FFPE section: 500-plex RNA + 18-plex protein + fluorescent H&E at subcellular resolution. Whilst not super exciting, the angle is throughput: 128 samples with 40 cm² per run, roughly 10× most competitors — squarely aimed at translational/clinical cohort work. Note also an in-situ-sequencing “Direct-Seq” mode for clonotypes/mutations slated for Early Access in H2 2026.

APR26 — 10x Genomics announced Atera, a brand-new in-situ instrument promising whole-transcriptome (~18,000 genes) spatial at single-cell sensitivity, on FFPE and fresh-frozen, with a >5 cm² imageable area. List price $495,000 with pre-orders now being taken; shipping H2 2026. On 10x’s own numbers it’s ~4× Xenium throughput and 2–3× sensitivity for the WT assay. At the moment the tech is human-only, with no proteins (yet).

NGS-based spatial transcriptomics

AUG25 — Stereo-seq OMNI for FFPE (a.k.a. Stereo-seq V2, Cell 2025) — STOmics swaps poly-T for random priming to capture total RNA (including non-coding and microbial) on FFPE at subcellular resolution, on those enormous nanoball-array chips; V1.1 reportedly doubles capture efficiency. It’s a BGI/MGI product running on DNBSEQ rather than Illumina chemistry, so in practice access means Complete Genomics/MGI or a service provider, plus the geopolitical overhang we return to below.

JUN26 — Illumina launched StrataMap (formerly the “Illumina Spatial Solution” teased at AGBT 2025). It’s a sequencing-based capture array with ~1µm features and a 7.5 cm² capture area, read out via sequencing (aka NovaSeq/NextSeq to keep the solution within the Illumina family). And it’s whole-transcriptome (poly-A capture, picking up non-coding RNA and pseudogenes), claiming ~2× the genes per sample of probe panels. The catch: fresh-frozen only at launch; FFPE isn’t due until 2027. Read it as a Visium HD competitor that trades FFPE for resolution and a greater capture area.

Spatial beyond spatial transcriptomics

JAN24 — AtlasXomics / Spatial epigenomics – The leading commercial route to spatial ATAC / CUT&Tag remains AtlasXomics, the Yale spin-out commercialising DBiT-seq. It’s sold as microfluidic chips, reagent kits, and the AtlasXpress instrument (and as a service), with an EpiCypher partnership for spatial CUT&Tag. Resolution is pixel-based (tens of microns), so it complements rather than competes with subcellular RNA imagers.

APR24 — Who are Element (Biosciences)? A fair question, since by origin they’re not a single-cell/spatial company. Element is a San Diego sequencing firm (founded 2017) whose AVITI benchtop sequencer — built on “avidity” base chemistry — has been the most credible mid-throughput challenger to Illumina. Their relevance here is AVITI24 + Teton CytoProfiling: using the sequencer itself as an imager to read out RNA (~350-plex) + protein (~50-plex) + phospho-protein + morphology on up to ~2M cells per run, with <1 hr prep and next-day results. The crucial caveat is that Teton profiles cultured/adherent cells and cell suspensions deposited on the flow cell — and not FFPE or fresh-frozen tissue sections. It’s high-content single-cell cytoprofiling, not a tissue-spatial Xenium competitor. Spatial on tissue via AVITI24 is on Element’s 2026 roadmap, but not shipping. AVITI24 itself is shipping (~$424k), with a certified-service-provider route opened DEC25, and a higher-throughput sequencer (VITARI) on pre-order for H2 2026.

FEB25 — Pixelgen extended Molecular Pixelation with the Proximity Network Assay (PNA) and launched the Proxiome kit: an optics-free, sequencing-based method that builds nanoscale (~50 nm) maps of ~155 surface proteins on individual cells via antibody-oligos and rolling-circle amplification — i.e., protein interactomes without a microscope. A genuinely new modality, commercially available as a kit. Current applications appear focused on T cells to help generate a next generation of anti-PD-1/PDL-1 treatments.

MAY26 — Survey Genomics — Some folk may have seen the preprint by scTrends coauthor and Arc Institute’s David Lara on their collaboration with Survey Genomics. Essentially, by pre-loading a nanowell chip with position-encoded DNA barcodes that transfer onto intact whole cells in a tissue section; the tissue is then dissociated and run through any standard single-cell workflow, so each cell carries a low-resolution spatial address while staying intact for downstream RNA/protein/TCR/CRISPR. For David’s work on in vivo perturb-seq, this massively scales up identifying edited regions of tissue and observing the macroscopic morphological changes. Important caveat: as of June 2026 it’s pre-commercial — the website is an interest form, not a catalogue.

The scTrends take: It’s great to see the space heating up. However, if we were to be so bold…

Singular Genomics hasn’t been around long enough for there to be enough gossip on data quality/user experience to ruminate, so it’s quite hard to have an informed opinion in this regard.

The Bruker/NanoString is old news now, and it feels like 10x Genomics’ Atera platform is being released to demonstrate that they’re not behind from a capabilities perspective. When you look into the capabilities between both companies (Bruker vs 10x Genomics), the CosMx data shows transcripts per cell maxing out at around ~1400 for their 6k panel and ~2000 for their whole transcriptome solution, whereas Xenium’s 5k panel tops out at ~1300 for their 5k panel (marginally more efficient), but their Atera whole transcriptome solution tops out at ~2100 transcripts per cell. So perhaps there’s a small edge for 10x Genomics, but hardly a side-by-side comparison.

So why are we even doing all of this? It sounds like a cliche, but our bet is that it is (hypothesized) new demand originating from AI applications. Consider the concept of transfer learning, aka, can you reuse ML models across similar applications/use cases? Multimodal imaging-based ST generates loads of data for various tasks (check also NOETIK.ai’s blog), so having indication-specific probe sets for each use case (e.g., breast vs lung vs brain etc) will be inherently limiting if you want to leverage data from across multiple organs.

Going forward… Our personal view is that imaging-based ST is probably the best route forward for clinical applications. This is primarily driven by large capture areas (not sensitivity) because it’s hard to know if your biopsy/resected tissue perfectly captures the relevant bit of disease pathology. However for research applications, there’s probably a lot more road for NGS-based ST. Illumina has shown that engineering ~1µm spots is technically possible, but as we’ve seen from internal research and other publications, if we go beyond poly-A capture, we can uncover huge amounts of novel biology — watch this space to hear it first (warning, preprint incoming).

Other new single-cell products:

NOV24 – CS Genetics SimpleCell — a brand-new, genuinely instrument-free scRNA-seq using proprietary “kinetic confinement” barcoding (not droplets or split-pool), same-day cells-to-sequencer, in 8/16/96-sample kits at <$500/sample. Shipping (96-plex from JUL25).

FEB26 – Atrandi Biosciences — the semi-permeable-capsule Onyx workflow added 170µm and 300µm capsule kits (FEB26) for spheroids/organoids and is pushing single-cell DNA+RNA co-profiling. Multi-step single-cell chemistry remains the differentiator.

Platform extensions:

JAN25 – Illumina Single Cell 3′ (ex-Fluent/PIPseq) — Illumina closed Fluent (JUL24) and relaunched PIPseq as “Illumina Single Cell 3′ RNA Prep” (JAN25) in T2–T100 kit sizes.

Ongoing – Incremental additions: 10x’s GEM-X chemistry (more cells/lane, lower cost) and the new Flex Apex (plate-based multiplexing, up to 384 samples; OCT25); BD Rhapsody OMICS-One WTA; Mission Bio Tapestri adding a targeted DNA+RNA assay (ASH, NOV25, waitlist); and Singleron’s Tensor automation and MobiuSCOPE.

Market news

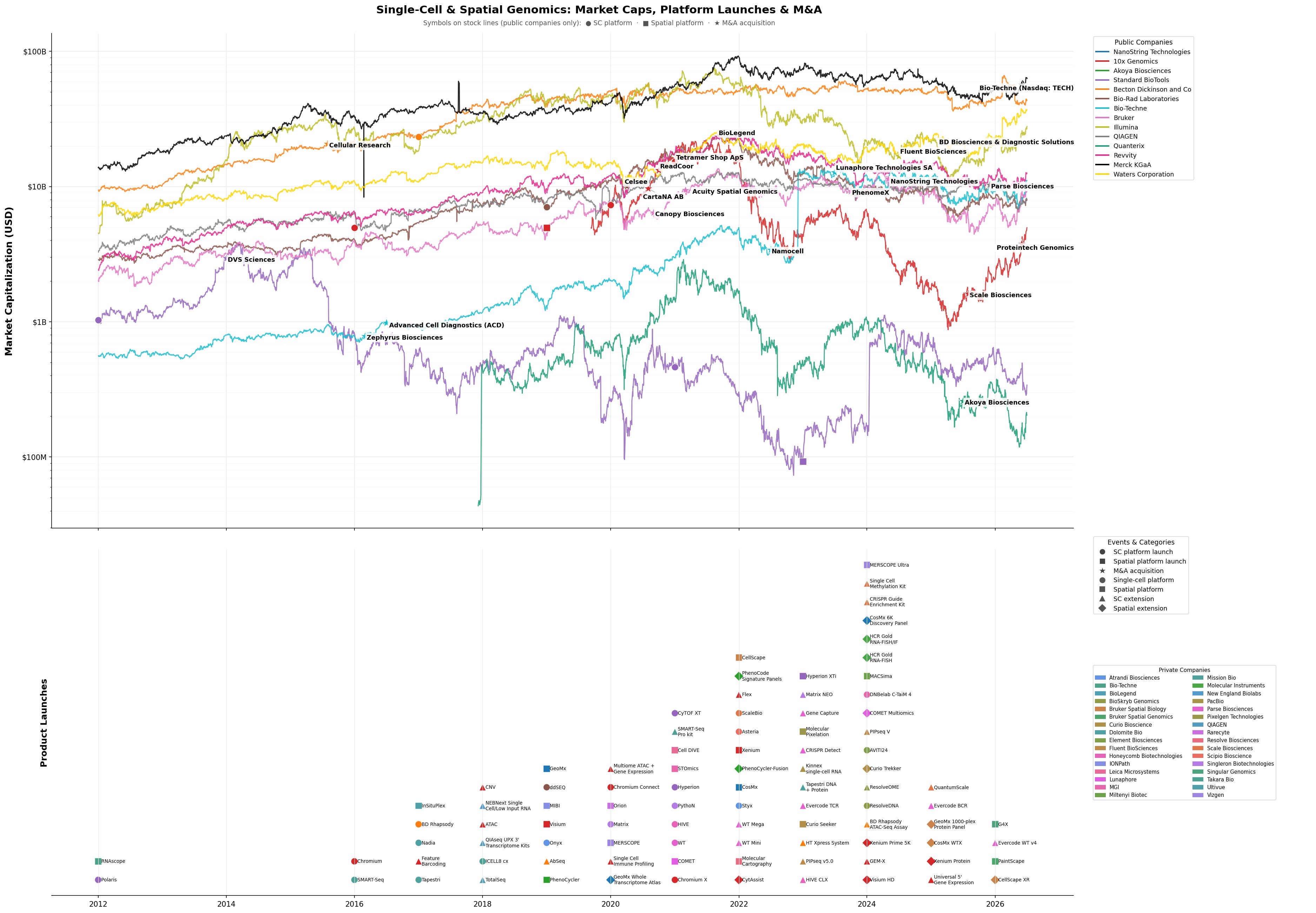

You can follow stock prices, M&A actvity and product launches in the graphic below, or download an interactive version here.

Combinatorial-indexing buy outs

AUG25 — 10x Genomics agreed to acquire Scale Biosciences (~$30M upfront + milestones), folding Scale’s QuantumScale “microwell-within-a-well” barcoding (millions of cells per run, ~1 cent/cell, <$100/sample) and ScalePlex multiplexing into the Chromium franchise. QuantumScale RNA kits began shipping in early 2025 and underpin CZI’s billion-cell ambitions.

NOV25 — QIAGEN agreed to acquire Parse Biosciences (~$225M + up to $55M milestones; closed DEC25). Parse’s Evercode split-pool now scales to ~5M cells (Evercode Penta), has added probe-free whole-transcriptome from FFPE, and runs >10M cells per experiment via its GigaLab service.

So both leading instrument-free challengers are now owned by incumbents! A notable inversion of the scrappy-upstarts-vs-10x framing from our earlier posts. On the Parse litigation we covered: it resolved largely in Parse’s favour on gene expression (PTAB invalidated the asserted WT claims, FEB25 post), though 10x did secure a consent injunction blocking Parse’s planned ATAC products.

Other M&A

OCT24 — Vizgen merged with Ultivue, then raised $48M to push MERSCOPE toward profitability.

DEC24 (closed FEB25) — Deerfield took Singular Genomics private.

JAN25 (closed JUL25) — Quanterix acquired Akoya (PhenoCycler), ultimately a cash-heavy, sharply reduced deal — distressed-asset spatial consolidation.

JAN25 — Takara acquired Curio (Seeker/Trekker). Takara has since launched Curio Trekker FX, bringing instrument-free single-cell spatial to FFPE (OCT25) and closing the line’s biggest gap.

JUL25 — Waters agreed to merge with BD’s Biosciences & Diagnostic Solutions business — the unit that houses the BD Rhapsody single-cell platform — in a ~$17.5B Reverse Morris Trust deal. BD spins the business out to its shareholders and merges it into Waters (BD holders ~39%, Waters ~61%, plus ~$4B cash to BD). Announced 14JUL25; expected to close ~9FEB26.

JAN26 — Illumina acquired the SomaScan proteomics business from Standard BioTools ($350M + milestones), part of a broader pivot to multiomics/proteomics.

JUN26 — Merck KGaA (Darmstadt) agreed to acquire Bio-Techne for $73/share cash (~$11.3B, a 36% premium) — its largest life-science deal since Sigma-Aldrich (2014), and is expected to close late 2026/early 2027. Bio-Techne brings RNAscope (ACD), the Lunaphore COMET spatial-proteomics platform and Namocell single-cell tools into the fold.

And the exits, which the spec table now reflects: Scipio Bioscience (Asteria) ceased operations (SEP24); Bio-Rad’s ddSEQ single-cell line is being discontinued; and Resolve Biosciences has gone conspicuously quiet — not reported bankrupt or acquired, but with no visible 2025–26 product activity.

Partnerships & data announcements

JUN25 — Gingko Bioworks as part of it’s ‘data points’ initiative publishes a pre-print on it’s scaled bulk 3’ counting DRUG-seq workflow for cell type perturbation, with claims in the pre-print claiming superiority vs other single-cell virtual cell datasets from companies such as Tahoe (Parse Biosciences)

DEC25 — Parse Biosciences announce a 10M cell cytokine screen in PBMCs in collaboration with the Theis Lab. The size of the dataset is clearly meant to appeal to model builders.

JAN26 — 10X Genomics enters clinical workflows via partnerships with both the Dana-Farber Cancer Institute and Brigham & Women’s Hospital. As part of this work, 10X Genomics will establish a CLIA lab to support future diagnostic expansion, with a focus on autoimmune disease.

JAN26 — Illumina (post its acquisition of Fluent Biosciences) announces a 5B-cell virtual cell data generation initiative and enters discovery alliances with pharmaceutical companies such as Elily Lilly, Merck and AstraZeneca. This highlights the growing trend of scaled hardware companies vertically integrating into both preclinical and clinical disease insights, as well as datasets for AI.

The scTrends take: Given depressed NIH budgets and an increasingly stormy geopolitical climate (e.g. no growth for Western Companies in China), tools vendors are becoming increasingly zero-sum in their approaches to driving revenue growth. This is manifesting as a wave of distressed or low-cost bolt-on M&A: Bruker, Danaher, Thermo, QIAGEN, Illumina and now Merck KGaA. It’s also manifesting as the scaled tools company beginning to explore how they vertically integrate to capture pharma discovery alliances, diagnostics, and potential AI data revenue. This places several of these companies in an interesting position whereby they may begin to compete with their own customers.

Litigation

A clean narrative arc this cycle. 10x settled its spatial disputes for cash + royalties — Vizgen (5FEB25, ~$26M) and Bruker/NanoString (12MAY25, ~$68M + royalties, ending US, German and UPC proceedings) — and is settling with Curio (now Takara). Then it pivoted up the stack:

OCT25 — 10x + Roche + Prognosys sued Illumina across nine patents covering both spatial (the StrataMap technology) and single-cell. This is the most strategically consequential dispute of the period: the spatial-tools leader now litigating directly against the sequencing incumbent that just entered its turf.

MAY26 — 10x + Harvard sued Element (AVITI24/Teton) on four patents (the ReadCoor/Church portfolio), the same day the Curio trial was stayed for settlement.

The pattern: monetise the spatial IP via settlement-and-coexistence, then enforce against the sequencing/multiomics layer (Illumina, Element) encroaching from below.

Aside: The floor under everything: sequencing got cheaper

Not strictly single-cell or spatial, but it’s worth mentioning movements in the sequencing market:

Ultima Genomics UG 100/Solaris pushed toward an ~$80 genome (~$0.24/M reads) and anchors the CZI Billion Cells and Tahoe-100M datasets.

Roche SBX (Axelios) — Sequencing-By-Expansion, detailed at AGBT 2026: $750k instrument, pre-orders open, formal launch summer 2026, promising ~$150 genomes. Roche’s serious re-entry — and, not coincidentally, 10x’s co-plaintiff against Illumina.

Element VITARI (pre-order, H2 2026) and Illumina’s NovaSeq X transition round out a genuinely contested sequencing market for the first time in years.

Geopolitics: the BIOSECURE Act passed (DEC25); with MGI/BGI already on the DoD’s 1260H list, the cheapest sequencing option (DNBSEQ) — and by extension Stereo-seq’s readout — faces a chilled US market regardless of technical merit.

Making this a living review

As ever, the detail lives in the resources we keep updated for anyone to use. Spotted something we’ve missed or gotten wrong? That’s the point of a living review — drop a note in the comments. Contributors from technology developers are welcome, providing you declare conflicts upfront!